Time to review your governance arrangements

Governance is one of the hot topics for charity trustees’ agendas. As a result of various events in the sector, as well as general good practice, it is timely for all charities to undertake an internal health check and take a look again at their governance arrangements.

What is good governance?

It is difficult to find a clear definition of effective governance. From the Financial Conduct Authority consultation paper Effective corporate governance (FCA-CP10/3, 2010) I can highlight a few key terms:

- Oversight and challenge.

- Delivering an agreed strategy.

- Clear understanding of the related risk appetite; a robust control framework.

- Monitoring outcomes.

These then form the outputs of good governance arrangements.

Several governance frameworks

There are several frameworks for governance and many similarities between them. The UK Corporate Governance Code is used to support governance in the UK’s top companies and its principles can apply just as well to charities.

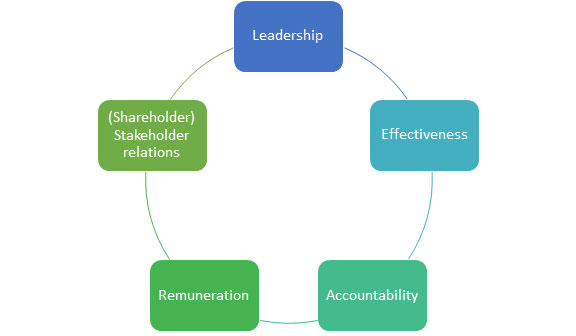

LEADERSHIP – the principles of leadership are also embodied in the Voluntary Sector Good Governance Code (Good Governance: A Code for the Voluntary and Community Sector, 2010). According to this an effective board will provide good governance and leadership by:

- Understanding their role.

- Ensuring delivery of organisational purpose.

- Working effectively both as individuals and a team.

- Exercising effective control.

- Behaving with integrity.

- Being open and accountable.

A board should have the right skills and experience to support the charity. This includes an understanding of both its own strategic role and the "on the ground" activities of the charity so that they provide strategic direction, challenge and oversight.

EFFECTIVENESS – a board of trustees cannot understand how effective it has been if there is no evaluation and review of the board, its composition, activities and impact. Trustees should consider regular, if not annual, self-evaluation both of the main board and the audit committee, if there is one (Deloitte Charity Audit Committee performance evaluation: self-assessment checklist).

Succession planning is another key to effectiveness, as the necessary challenge between executive and non-executive can be compromised or relaxed by familiarity. The trustees need to continually manage the balance between experience and those new to the organisation.

ACCOUNTABILITY – the board of trustees must understand the business model, the impact of that model on the risks effecting the charity, and the risk appetite of the charity. The board needs good quality management information to enable it to challenge the direction, activities and outcomes and ensure that charities are meeting their charitable objectives and delivering the agreed strategy.

The trustees should understand and test the control framework in place to ensure it is robust and effective.

REMUNERATION – it has always been a requirement for charities to disclose any remuneration paid to trustees and expenses claimed or paid on behalf of trustees. As the focus on pay in the private sector has increased so there has been a similar interest in the pay of charity management, particularly that of charities’ chief executives.

Description of pay arrangements

As a new requirement under the FRS102 (Financial Reporting Standard) and FRSSE (Financial Reporting Standard for Smaller Entities) SORPs (Statement of Recommended Practice), the trustees must include in their annual reports a description of the arrangements for setting the pay and remuneration of the charity’s key management personnel and any benchmarks, parameters or criteria used in setting their pay. Further they must include the aggregate payments made to the key management personnel.

The SORP states that charities may choose to include disclosure of remuneration and other benefits paid to their key management personnel on an individual basis. How charities will typically report under the new requirements is not yet clear.

STAKEHOLDER RELATIONS – although shareholder relations are subject to specific requirements in the corporate governance code, this tweaked heading provides a useful prompt for trustees to consider their impact on those around them - funders, supporters, volunteers, beneficiaries.

The Charity Commission has recently consulted on guidance on fundraising (Charity fundraising: a guide to trustee duties, 2015). which challenges trustees to review their approach to fundraising and reassess their controls and understanding of their charity’s activities, and promotes the new Code of Fundraising Practice (Institute of Fundraising: A Code of Fundraising Practice).

Charity trustees should consider and monitor not only the outcomes of their activities and the impact on beneficiaries, but also the potential impacts on donors and supporters as they carry out their activities.

The role of the board

The remit of the board of trustees is broad and each trustee brings their unique experience and viewpoint to the table. Each part of the governance framework cannot be delivered in isolation. It must be a coherent whole. Therefore, the skills of each trustee need to be integrated, understood and appropriate to their role in support of the work of the board.

The board needs to set a strategy and understand the business model and risks. It needs to establish the boundaries of control, through clear delegation. Further the board must oversee robust monitoring controls and require reporting and assurance on the systems operating. It is the role of the trustees to challenge any and all parts of the operation from the strategies for fundraising and investment, to charitable activities grants and other spending. They should then monitor the outcomes against their original plan.

Now is the time for charity trustees to step back and assess their governance arrangements. Each trustee needs to be confident that they understand:

- Their role.

- How they and their charities operate.

- Whether and how management and strategy are integrated and challenged to provide effective leadership and good outcomes.